Planet Fitness (PLNT)·Q4 2025 Earnings Summary

Planet Fitness Beats Q4 Estimates But Guidance Disappoints, Stock Falls 5%

February 24, 2026 · by Fintool AI Agent

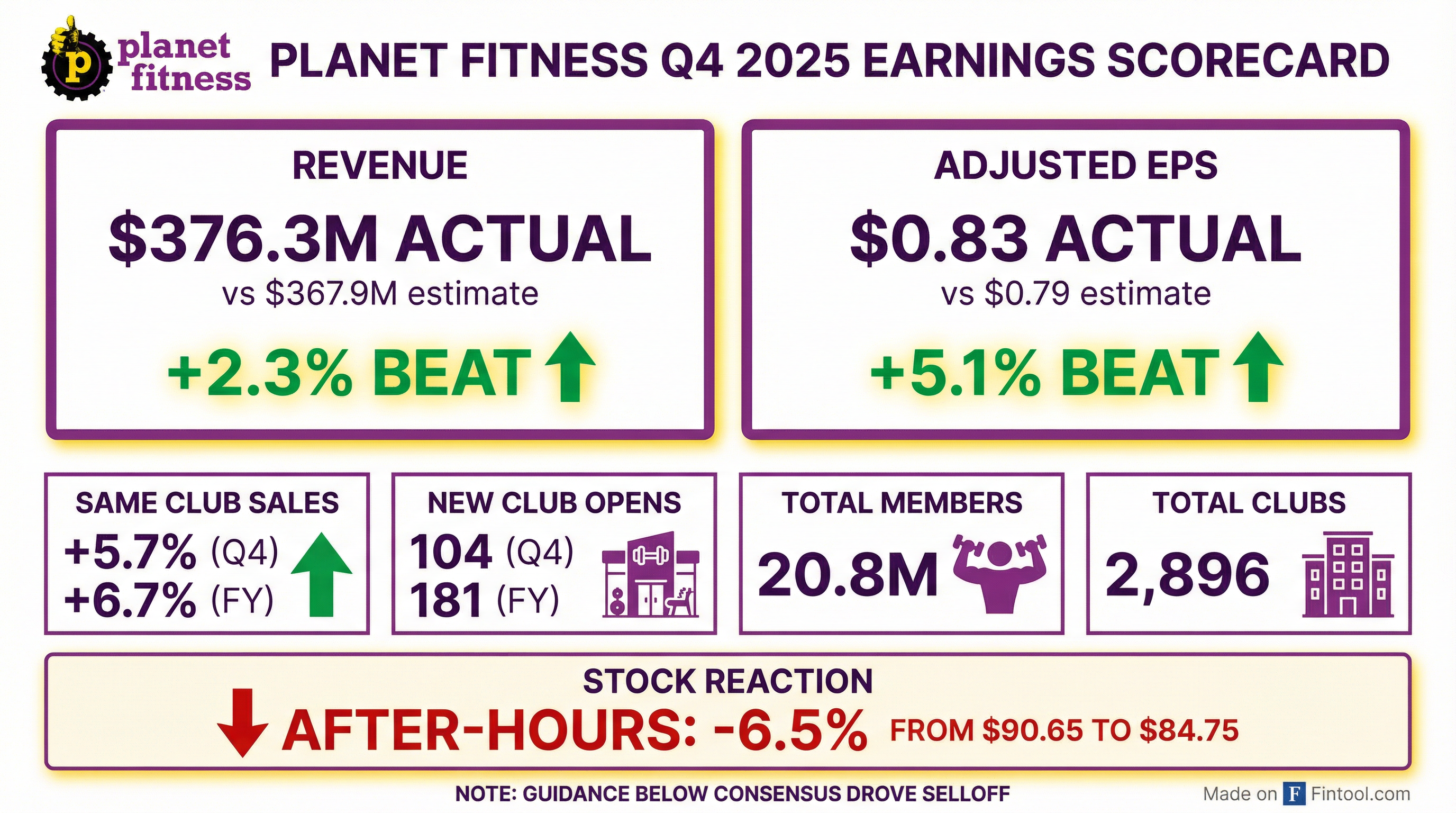

Planet Fitness delivered a solid Q4 2025 with revenue of $376.3M (+10.5% YoY) and adjusted EPS of $0.83 (+18.6% YoY), beating analyst expectations on both metrics . However, shares tumbled 5% after-hours to $86.08 as FY 2026 earnings guidance came in roughly 5% below Street consensus, signaling that the company is prioritizing growth investments over near-term profitability. Management attributed near-term headwinds to January weather disruptions impacting ~2,000 clubs and a slight elevation in attrition during the first month of online cancellation anniversarying .

Did Planet Fitness Beat Earnings?

Yes — Planet Fitness beat on both revenue and EPS in Q4 2025.

*Values retrieved from S&P Global

This marks the 7th consecutive quarter of EPS beats for Planet Fitness, continuing a pattern of consistent operational execution.

Full Year 2025 Highlights

The company ended 2025 with approximately 20.8 million members and nearly 2,900 clubs globally . Q4 saw 104 new club openings—an all-time quarterly high .

Q&A Highlights: What Did Analysts Ask?

January Weather and Attrition Impact

CFO Jay Stasz addressed the two transitory headwinds that impacted January :

"About 2,000 clubs, based on our data, had some form of impact, and we saw a marked difference in the relative join volumes during the storm period. Since that time, for the markets that were impacted, we've seen a nice rebound, and then we've seen some very healthy join rates related to promotions we've run in February."

On elevated attrition in January :

"This was the first year of a high volume period with the ability to manage your membership with our messaging around cancel anytime. Maybe in January, it's more top of mind, just like fitness is. We have made some tweaks to our messaging in our digital platform around cancellation, and we have seen that the attrition rate has come in line in February with our expectations."

CEO Colleen Keating noted that full-year 2025 attrition remained well within historical norms at a "3 handle" annualized rate, and 34.8% of Q4 joins were rejoins .

Black Card Price Increase Timeline

When asked about timing, Keating indicated the Black Card price increase will come after peak join season :

"For competitive reasons, we're not being overly specific... Q3 obviously is our lower join quarter. That will give you an indication of when we're anticipating to roll that out."

The 2026 comp guidance embeds approximately 75% from rate and 25% from volume .

GLP-1 Partnership with Ro

The Ro partnership, launched in late Q4, is showing strong early traction :

"While it is still early days and too soon to run a victory lap, we can share that this has been our most successful Perks program yet, with high download and conversion."

Management cited research showing 50% of people who take a GLP-1 consider a gym membership, positioning Planet Fitness as the natural choice for first-time gym-goers concerned about muscle mass loss .

New Black Card Amenities Test

Keating shared firsthand observations from testing new Black Card Spa amenities :

"I tried a few of the new Black Card Spa modalities we're currently testing, including the dry cold plunge and the red light sauna. I spoke with members who were using the new amenities as well to hear their feedback, and it was resoundingly positive. We see an opportunity to drive both joins and upgrades, as well as enhance retention with these new amenities. It's our opportunity to democratize recovery and wellness, just as we did with fitness 30 years ago."

What Did Management Guide?

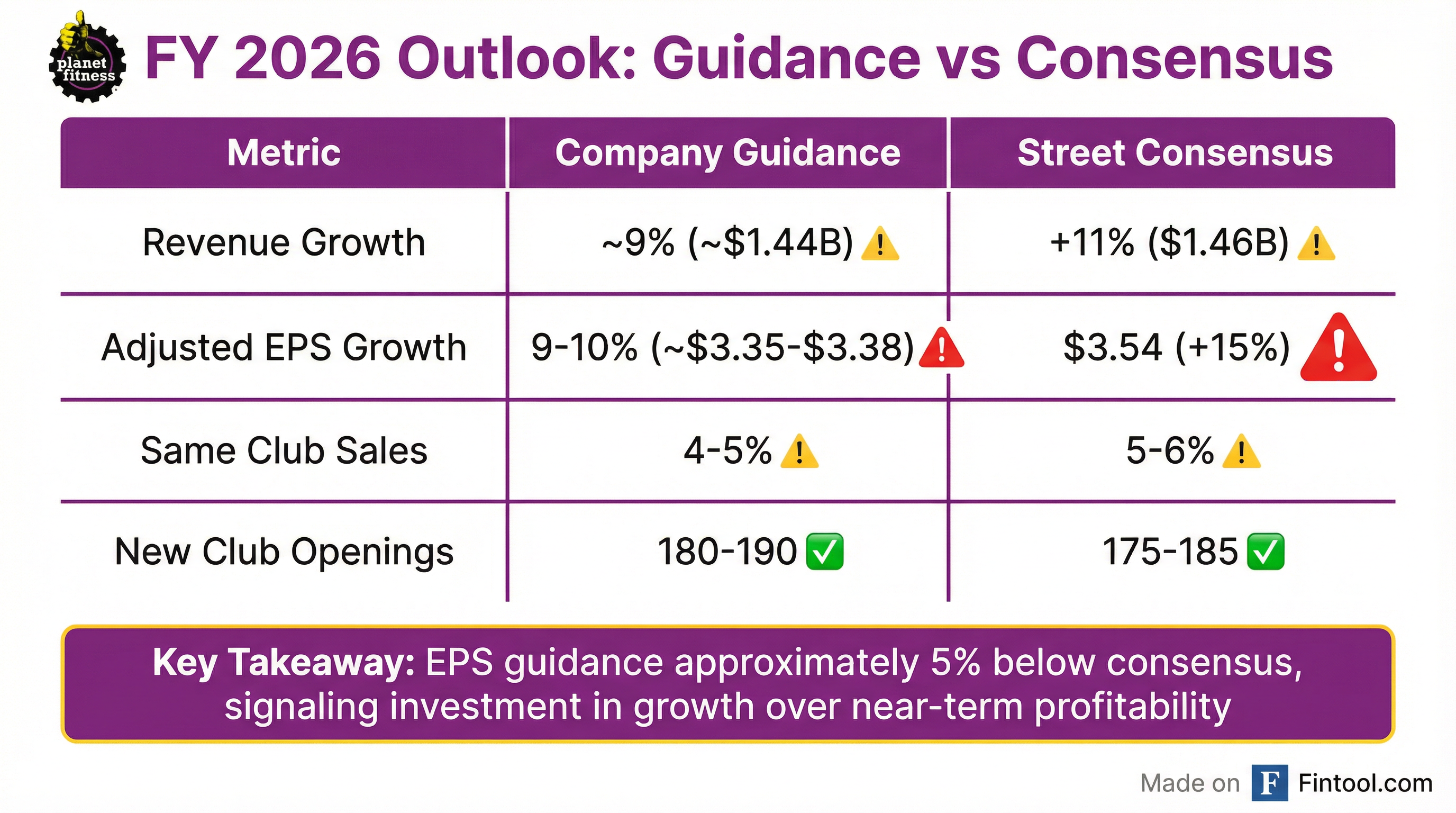

FY 2026 guidance came in below consensus, particularly on earnings.

*Values retrieved from S&P Global

Key Investment Areas Driving Guidance

CFO Jay Stasz acknowledged this is the "lowest growth year in our three-year algorithm" due to two primary factors :

- Extended equipment replacement cycle — Part of the new growth model rolled out in 2024

- California club sale impact — Q3 2025 sale of 8 corporate clubs reduces YoY comparisons

- CapEx increasing 10-15% — Corporate club buildout and relocations/remodels

- Net interest expense up ~$29M — Reflects 2025 refinancing at 5.4% blended coupon

- Spain operations — Marketing process underway to convert to franchise model

The deceleration in same-club sales guidance from 6.7% (FY25) to 4-5% (FY26) also reflects that the company is lapping the nationwide rollout of online member management in Q2 . CFO Stasz noted: "We expect lower comps in the first half, and we think about higher comps in the back half as a result of that" .

Management reiterated commitment to the 3-year growth algorithm laid out at Investor Day, expecting to "get back to those targets" in years 2 and 3 .

How Did the Stock React?

Shares fell ~5% after-hours despite the Q4 beat.

The stock is now trading near its 52-week low, down approximately 25% from its 52-week high. The selloff reflects investor disappointment with:

- FY 2026 EPS guidance ~5% below consensus — Adjusted EPS growth of 9-10% vs Street at +15%

- Same-club sales deceleration from 6.7% to 4-5%

- January transitory headwinds — Weather impacts and elevated attrition

- Net interest expense jump — ~$114M vs ~$85M in FY25

What Changed From Last Quarter?

Positive Developments

- Record Q4 club openings: 104 new clubs in Q4 alone—an all-time quarterly high

- Black Card penetration all-time high: 66.5%, up 260 bps YoY

- High School Summer Pass success: 3.7 million teen participants (+20%+ YoY), 8.3% conversion to paying members

- International milestone: Surpassed 1 million members and 200 clubs internationally

- Strong balance sheet: Cash and marketable securities of $607M

- Strong rejoin rate: 34.8% of Q4 joins were returning members

Areas of Concern

- January transitory headwinds: ~2,000 clubs impacted by storms, slight attrition elevation

- Same-club sales deceleration: Guidance of 4-5% for 2026 vs 6.7% achieved in 2025

- Interest expense headwind: ~$114M in 2026 vs ~$85M in 2025 from refinancing

- First-half comp pressure: Lapping online member management rollout in Q2

- California club sale lap: 8 corporate clubs sold in Q3 2025 creates YoY comparison drag

Segment Performance

Q4 2025 segment breakdown :

Equipment mix shift: Replacement equipment accounted for approximately 60% of total equipment segment revenue, compared to 58% in the prior year . For 2026, management expects reequipment to represent ~70% of segment revenue .

New club comp waterfall from CFO Stasz :

- Year 1 in comp base: ~40%+ comps

- Year 2: Low to mid-teens

- Year 3: Mid-single digits

- Beyond: Low to mid-single digits

Key Management Quotes

CEO Colleen Keating on 2025 performance :

"Our strong 2025 performance is a direct result of our discipline and focus on our four strategic imperatives. We ended the year with approximately 20.8 million members and a global footprint of nearly 2,900 clubs, reinforcing the quality of our member experience and our compelling value proposition. Anyone can get a great workout at Planet Fitness for an incredible value."

On member loyalty and rejoin trends :

"Mid 30% of our joins are rejoins. We know that when we're treating our members well and giving them the opportunity to manage their membership, they're coming back to us."

CFO Jay Stasz on the 3-year algorithm commitment :

"We knew that this year would represent the lowest growth year in the three-year algo. The intent was not that that three-year algo was an annual growth rate for each year... We see increases in both year 2 and year 3 of our growth algo to get back to the targets we laid out."

On Click to Cancel strategy :

"Strategically, we think this is the right thing to do from a member experience standpoint and from a de-risking the business standpoint... We are seeing lift in our digital conversions with the ability to cancel anytime."

Capital Allocation

Planet Fitness maintained an aggressive capital return program in 2025 :

Management expects ~80 million adjusted diluted weighted average shares outstanding for 2026 . The franchise/corporate split remains approximately 90/10, which management views as "a good balance given the four-wall profitability" .

Forward Catalysts & Risks

Catalysts to Watch

- Black Card price increase (Q3 2026) — Management indicated post-peak-join-season timing

- Spain franchise conversion — Banker engaged, "number of interested investors"

- New Black Card Spa amenities — Dry cold plunge, red light sauna in pilot; could drive upgrades/retention

- AI-enabled marketing capabilities — DCO, predictive churn model, AI-enabled CRM funded by NAF shift

- GLP-1 partnership expansion — Ro partnership showing "most successful Perks program yet"

- Second-half comp acceleration — Management expects higher comps in H2 after lapping member management rollout

Key Risks

- January attrition trend — First year of high-volume Click to Cancel; needs continued monitoring

- Equipment cycle timing — Reequip represents ~70% of segment revenue; extended replacement cycle pressure

- Interest expense headwind — ~$29M YoY increase from refinancing

- First-half vs second-half execution gap — Guidance assumes back-half-weighted improvement

- International execution — Spain still developing, Mexico entering new markets

Bottom Line

Planet Fitness delivered a solid Q4 2025 with beats on both top and bottom line, capping off a strong fiscal year with 12% revenue growth, 13% EBITDA growth, and 19% adjusted EPS growth. The 104 Q4 club openings—an all-time quarterly record—and Black Card penetration reaching 66.5% demonstrate the brand's enduring strength.

However, the 2026 outlook disappointed investors on multiple fronts: EPS guidance ~5% below consensus, same-club sales decelerating to 4-5%, and interest expense jumping ~$29M. Management attributed the soft start to January weather disruptions impacting ~2,000 clubs and elevated attrition during the first Click to Cancel anniversary—both described as transitory and now normalizing.

The bull case: Three-year algorithm commitment remains intact, Black Card price increase coming in Q3, GLP-1 tailwinds gaining traction with the Ro partnership, and new wellness amenities could drive upgrades and retention. The 34.8% rejoin rate and 6% lift in digital conversions from Click to Cancel suggest the member experience investments are working.

The bear case: 2026 is admittedly the "lowest growth year" in the algorithm, first-half comps face tough comparisons, and the Street needs to see proof that H2 acceleration materializes. The ~5% after-hours decline suggests investors are taking a show-me stance.

Related Reading:

Data sourced from Planet Fitness Q4 2025 earnings call transcript (February 24, 2026) and S&P Global Capital IQ estimates.